Pull up any pitch deck from an ad tech company five years ago and you'll find the word independent in it somewhere. It was a selling point. We're neutral, we work with everybody, your data is safe with us because we don't compete with you.

Good luck finding that pitch today.

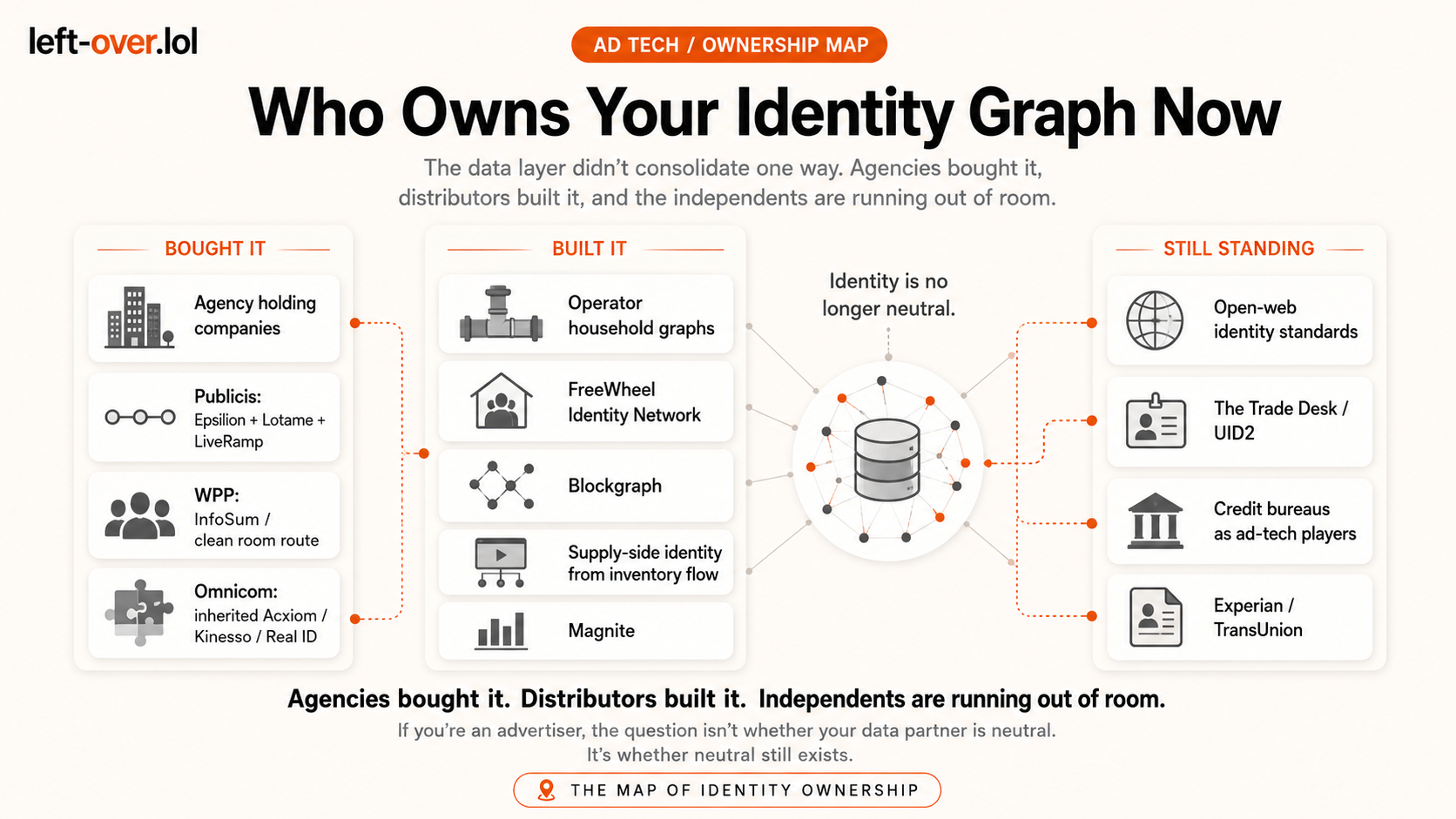

The data and identity layer of advertising, the plumbing that figures out who you are across your phone, your laptop, and your TV, has been quietly swallowed. Not in one big dramatic deal. In a steady drip nobody bothered to connect until it was basically done. And it happened two different ways, which is the part most people miss. Some companies bought their way in. Others built something the buyers can't touch.

The ones that got bought

Publicis is the aggressor. It bought Epsilon in 2019 for $4.4 billion, grabbed Lotame in early 2025, and just closed on LiveRamp for $2.5 billion. Stack those three and Publicis owns the deepest data operation in the agency world. Nobody else is close. Epsilon brought 2.3 billion consumer profiles. Lotame added an audience marketplace. LiveRamp is the part that connects it all to more than 25,000 publishers. The catch: LiveRamp was infrastructure the entire industry was built on, including Publicis's own competitors, who now have to decide whether they're comfortable running on rails their rival owns.

WPP went a different route. Instead of buying an identity graph, it bought InfoSum, a data clean room company, and folded it into Choreograph inside GroupM. WPP's pitch is that identity is dying anyway, so why buy a fading asset. They call it intelligence beyond identity. Translation: let the data sit where it is and connect to it instead of hoovering it all into one database.

Omnicom got the biggest prize almost by accident. When it absorbed IPG, it inherited Acxiom, one of the oldest and largest consumer data companies alive. Omnicom's data operation now claims 2.6 billion verified consumer identities and underpins roughly $73.5 billion in annual media spending. Acxiom brought Kinesso and Real ID along too.

The credit bureaus are in this game now, which should unsettle you a little. TransUnion bought Neustar for $3.1 billion and folded its OneID platform into TruAudience. Experian owns Tapad and a cross-device graph. The companies that know your credit score also help target your ads.

The ones building their own from data nobody can buy

Here's the part of the story almost nobody tells. While the agencies were busy buying, the companies that own the actual pipes were building. And what they're building is harder to compete with, because you can't acquire your way to it.

FreeWheel, owned by Comcast, runs the FreeWheel Identity Network. The thing that makes it different is the source. Most ad tech identity is probabilistic, which is a polite word for educated guessing. FreeWheel's is deterministic, anchored at the household level on Comcast's national footprint. It knows, because Comcast is the cable bill. The 2026 proof point is political: DSPolitical became the first political firm to run voter data through the FreeWheel Identity Network, activating first-party voter files across streaming for the midterms. FreeWheel also plays connector, interoperating with Blockgraph, Experian, LiveRamp, OpenAP, and TransUnion, so it's both a graph and a switchboard.

Blockgraph is the one that should make you sit up. It isn't owned by any single company. It's owned jointly by Comcast NBCUniversal, Charter Communications, and Paramount. Three of the largest TV distributors built a shared identity layer together and call it an Identity Operating System. It runs peer-to-peer, so each company keeps full control of its own data instead of dumping it into someone else's database. Charter's Spectrum Reach uses Blockgraph to do cross-screen attribution across its 16 million TV subscribers.

Magnite, the largest independent sell-side platform, is building identity from the supply side. Every impression that flows through it is a data point, and it's turned that into its own audience and identity offering. It's a different vantage point than the operators, but it's still a graph built from a position nobody else occupies.

The thing all three share: you cannot buy what they're sitting on. That's a moat the holding companies, for all their dealmaking, simply cannot acquire.

The ones still standing in the middle

This list is short, and it's getting shorter.

The Trade Desk is the big independent. Public, on NASDAQ, and openly betting against the holding companies with UID2, an open-source identity standard it's pushing as the currency for the open web. It says the word independent a lot, and at this point the word is doing heavy lifting.

Experian and TransUnion are technically nobody's property, but they own data and sell it. They're players, not Switzerland.

And that's basically the list.

Who's next, and the twist nobody's flagging

Here's where I'll stick my neck out.

On the buy side, the most acquirable assets left are the open-web identity players and the clean rooms. ID5, the European graph, is exactly what a WPP or Omnicom wants in order to claim a piece of the open internet without building it. 33Across and the cookieless crowd are in the same boat. Audigent and the curation-plus-data shops are attractive tuck-ins because they sit right at the seam between data and buying.

But the more interesting question is on the build side, and it ties straight back to the deals everyone's watching.

Blockgraph is co-owned by Comcast, Charter, and Paramount. Now look at the merger board. Paramount is mid-merger with Warner Bros. Discovery. Comcast bid on WBD, lost, and is sitting on cash. So the industry's shared identity backbone, the neutral household graph that three giants built together, is co-owned by companies that are actively at war over consolidation. If Paramount changes hands, what happens to its third of Blockgraph? Does a combined Paramount-WBD inherit a seat at the same table as Comcast, the company that just tried to buy the thing it's merging with? Nobody is asking that out loud yet. They should be.

The throughline is simple and a little bleak. Everyone looked at a future where Google and Amazon own the walled gardens and decided the only way to survive was to own identity. The agencies bought it. The distributors built it. The independents are running out of room.

If you're an advertiser, the question isn't whether your data partner is neutral. It's whether neutral is even a thing that still exists.