| Asset |

Year |

Outcome |

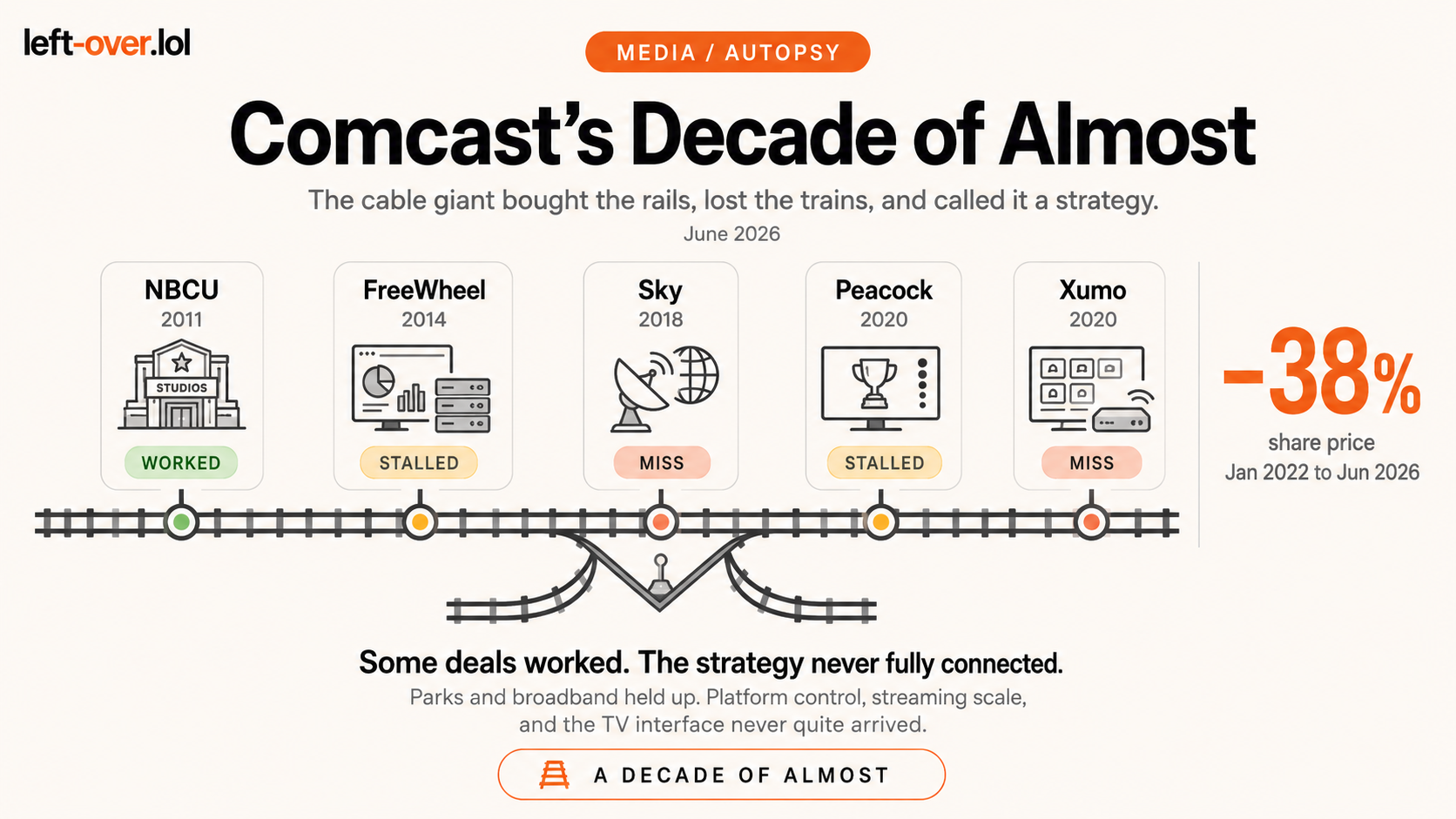

| FreeWheel |

2014 |

Stalled |

| Visible World |

2015 |

Stalled |

| Sky |

2018 |

Miss |

| Xumo |

2020 |

Miss |

| Peacock |

2020 |

Stalled |

| Beeswax |

2021 |

Miss |

| NBCUniversal |

2011 |

Worked |

| DreamWorks |

2016 |

Worked |

| Comcast Business tuck-ins |

2019-25 |

Worked |

The ad tech thesis aged out

FreeWheel was the right asset at the right time. 2014, before CTV advertising became the category everyone wanted to own. Comcast paid roughly $360 million for the premium video ad server, folded in Visible World for addressable TV, added Beeswax for the buy side, and assembled what should have been the most defensible independent stack in the market.

It didn't become that. A decade later, FreeWheel is solid infrastructure, widely deployed, quietly important, but it hasn't compounded into something that rivals what Google Ad Manager does for the open web. The structural problem was always the same: FreeWheel needs to be a neutral platform for publishers who compete with Comcast. That tension doesn't go away just because the product is good. Comcast never fully solved it, and the stack has been more incremental than transformative.

Beeswax, the buy-side piece acquired through FreeWheel in 2021, was supposed to close the loop. It hasn't cracked the top four DSPs by any meaningful measure. The full-stack vision, Comcast owning the sell side, the buy side, the audience data, and the measurement layer, is technically there on paper. Commercially, it hasn't mattered the way it was supposed to.

Xumo is a seatbelt, not a vehicle

Three product launches. One brand. Zero market leadership. Xumo Play, Xumo Stream Box, Xumo TV, a joint venture with Charter that exists primarily to ensure Comcast and Charter are not completely at the mercy of Roku, Amazon Fire TV, and Samsung in the living-room interface war.

That's a legitimate defensive concern. It does not make Xumo a business. If Roku disappeared tomorrow, Xumo still wouldn't be the first call for most consumers. It's the store brand in a category where the name brands have ten-year head starts and vastly superior content discovery. Insurance, not strategy.

Sky: the deal that should have been someone else's problem

The clearest financial disaster in Comcast's recent M&A history didn't involve ad tech. It involved winning a bidding war against Disney, which should have been the warning sign, to pay roughly 17.28 pounds per share for a European satellite TV operator in 2018.

Sky is a genuinely excellent company. Brand equity, sports rights, streaming product DNA, 17.6 million residential customers across the U.K. and Italy. It also relies on a distribution model, satellite pay TV, that was already getting structurally repriced when Comcast wrote the check. An $8.6 billion noncash impairment in 2022. Doubled operating losses in the U.K. Flat revenue. Comcast bought a great operator at exactly the wrong moment in the cycle and paid a bidding-war premium to do it.

Peacock is a sports app in a trench coat

44 million paid subscribers and $5.4 billion in 2025 revenue would be a respectable streaming business if the subscriber base wasn't so transparently tethered to sports rights. Pull out the NFL Sunday Night Football window, the Premier League, and the Olympics, and the retention picture looks substantially different.

Comcast built Peacock as a catch-up project. It was always behind Disney+, HBO Max, and Netflix by the time it launched in 2020. Losing control of Hulu, which Comcast inherited through NBCU and ultimately sold to Disney for roughly $9 billion, made it more so. The streaming scale Comcast needed in 2020 was sitting in Hulu's subscriber base. What they got instead was a platform that lives and dies on whether you care about the Premier League.

NBCU worked, but not quite how they planned

To be fair, NBCUniversal is Comcast's best modern deal by a distance. The parks, studios, and sports properties have compounded. Theme Parks alone hit $9.8 billion in revenue in 2025, up 14 percent year over year. Epic Universe opened in May 2025 as the most significant theme park launch in a generation. DreamWorks IP, Shrek, How to Train Your Dragon, found a second life inside the parks even as the studio output stayed uneven.

But the cable-network sleeve of the deal aged the way all cable networks aged. MSNBC, CNBC, USA, E!, SYFY, and the rest got separated into a new company called Versant in January 2026. Comcast didn't buy bad assets. They were excellent assets in 2011. The problem is that the bundle they bought contained both crown jewels and melting ice cubes, and sorting one from the other took fifteen years of subscriber losses to resolve.

Comcast didn't buy bad assets. They were excellent assets in 2011. The problem is that the bundle contained both crown jewels and melting ice cubes, and sorting one from the other took fifteen years.

The pattern underneath everything

Comcast is good at buying things it can run through existing infrastructure, parks, pipes, enterprise networking. The Comcast Business tuck-ins, Masergy, Nitel, Deep Blue, BluVector, are unglamorous but they helped build a $10 billion-plus enterprise revenue line with almost no attention.

Where it struggles is acquiring exposure to business models that were already being repriced. Sky was satellite pay TV at the end of the satellite pay TV era. The cable networks were cable networks at the end of the cable era. The ad tech stack is premium-video infrastructure in a market where the real leverage is in first-party data and identity, which Comcast has but hasn't yet turned into anything clear.

The deals Comcast didn't get, Roku, Fox, a controlling stake in Hulu, would have given it platform distribution or streaming scale. The ones it got gave it content, infrastructure, and a European broadband operator with structural headwinds. That's not a failure. It's a decade of almost.

Did any of this return value to shareholders?

The honest answer is: not really, and the stock says so.

Comcast shares traded around $57 in early 2022. By mid-2026 they sit closer to $35, a decline of roughly 38 percent over four years while the broader S&P 500 ran significantly higher. This is not a blip. It is a sustained, prolonged re-rating of what the market thinks Comcast is worth.

The Sky impairment alone wiped $8.6 billion in value in a single quarter in 2022. That's not a rounding error. That's a number that sits in the company's history as evidence that the most expensive acquisition Comcast made in the last decade was made at the wrong time, for the wrong price, in a business already in structural decline.

Broadband, which for years was the one business Wall Street trusted unconditionally, started losing subscribers. Comcast reported its first meaningful broadband subscriber losses as fixed wireless alternatives from T-Mobile and Verizon pulled customers away. The market had priced Comcast as a broadband monopoly. When that story cracked, so did the premium.

Peacock is losing money at scale. Comcast has committed billions to a streaming platform that trails Netflix, Disney+, Max, and Paramount+ in subscriber count and cultural relevance. It is funding that gap out of cash flows from a cable business that is itself shrinking. Investors are essentially being asked to subsidize a streaming catch-up play with no clear end date, in a market that has already picked its winners.

The ad tech investments, FreeWheel, Beeswax, AudienceXpress, have not translated into a revenue line that moves the needle at Comcast's scale. Collectively they are a rounding error against a company doing $120 billion in annual revenue. The thesis was right. The execution produced infrastructure, not a business.

And the Versant spinoff, separating the cable networks into their own entity in early 2026, is the market's final verdict on what that portion of the NBCU acquisition was worth. Spinning out MSNBC, CNBC, USA, and the rest is the corporate equivalent of admitting you bought a house and the back half is now a liability.

None of this means Comcast is broken. The parks business is genuinely excellent. Comcast Business is a $10 billion revenue line that gets almost no credit. The core connectivity infrastructure, whatever its current subscriber trends, is still essential in a way few assets are.

But for shareholders who have held through the Sky deal, the Peacock build, the broadband slowdown, and the cable-network spinoff, the returns have been poor. The M&A playbook that looked coherent on paper in 2018, buy content, buy Europe, build streaming, control the ad stack, produced a company that is harder to value, carrying more debt, bleeding legacy subscribers, and funding a streaming platform that most people open once a week to watch a soccer game.

That is what the stock is pricing. Not catastrophe. Just the slow accumulation of deals that made strategic sense at the time and didn't compound the way they were supposed to.