Streaming / Deep Dive

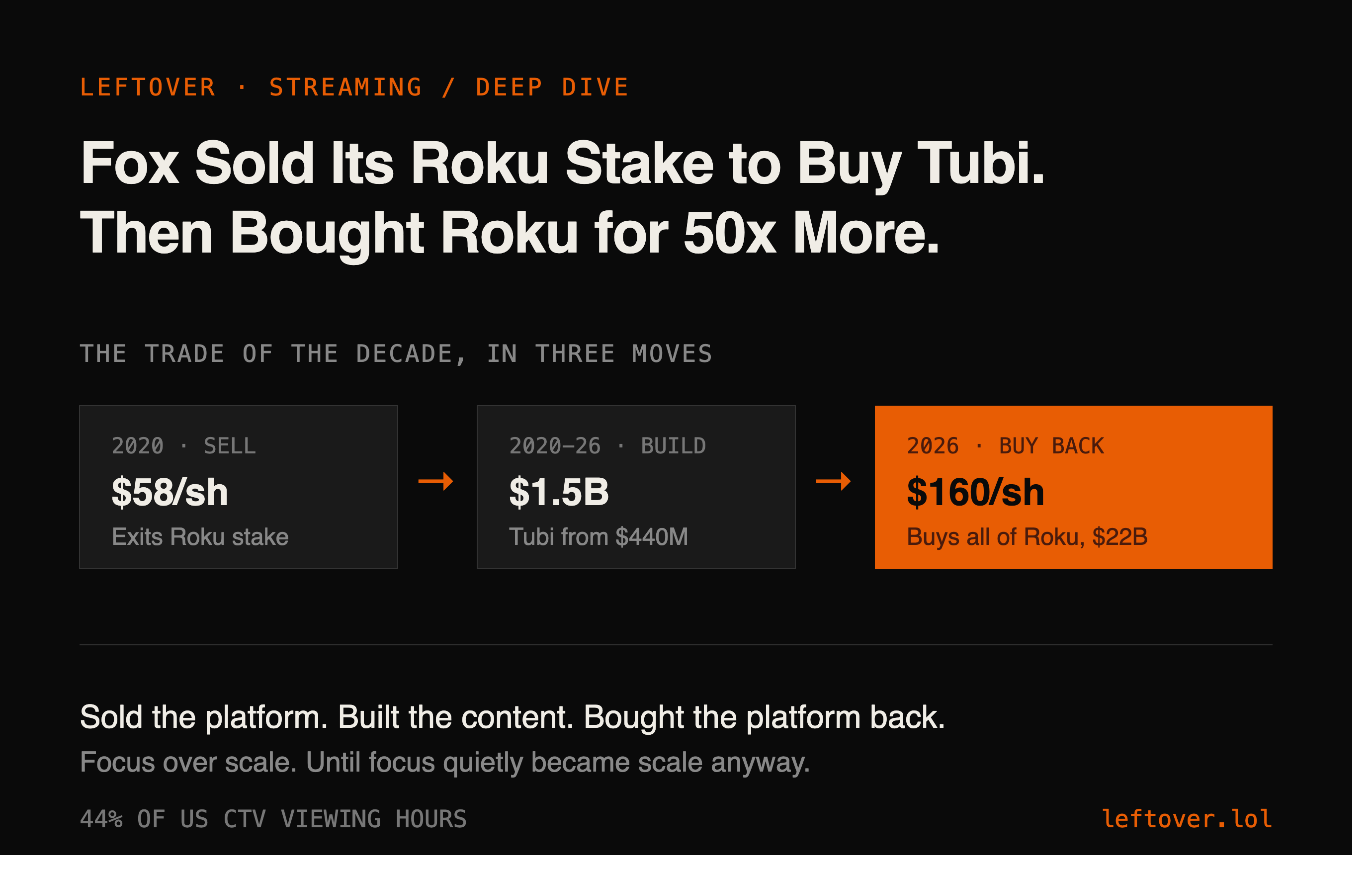

In 2020, Fox cashed out of Roku to fund a free streaming bet. Six years later, it bought Roku for $22 billion. The irony isn't lost on anyone. But the strategy was more deliberate than it looks.

Most people in the industry remember Fox selling its Roku stake in 2020 as a mild curiosity. A company quietly exiting a position to fund a new acquisition. What nobody said at the time: Fox wasn't selling Roku because it didn't believe in Roku. It was choosing where it wanted to own value in the streaming supply chain, and it had concluded that content beat platform.

The theory was straightforward. In a world where streaming explodes, must-watch content is worth more than distribution. If you own live sports and news, the platforms come to you. You don't need to own the pipe when everyone needs your water. Tubi, a free ad-supported service with no content production costs, was the bet on that theory. Fox could own the content and distribute it everywhere, rather than own the platform and negotiate with every content provider.

Tubi validated the bet faster than anyone projected. The $440 million acquisition hit profitability ahead of Fox's own internal timeline. Revenue approaching $1.5 billion in fiscal 2026. One hundred million monthly active viewers. Thirteen billion hours of content consumed annually. Those metrics justify the Roku acquisition not as a reversal of the original theory, but as its logical extension.

Fox didn't buy Roku because the original Tubi theory was wrong. It bought Roku because the theory worked well enough to justify owning both sides of the trade.

The ad tech logic is what most coverage is missing. Roku's data on viewing behavior is unparalleled. Connected TV devices generate granular signals about attention, completion, switching behavior, and content preference that no other platform can match at scale. Married to Fox's sports and news audiences, the most valuable inventory in advertising, that data creates targeting and attribution capabilities that programmatic buyers have been trying to construct for years.

The irony of the Roku stake sale is real. Fox exited a position that would have been worth considerably more in 2026 than it was in 2020. But the trade was not irrational. The Tubi revenue and the strategic position it created may be worth more than the unrealized Roku appreciation would have been. The more interesting question is whether any other media company has the discipline to execute a trade like this over a six-year horizon without reversing course when the first-year numbers look bad.

Full interactive version: leftover.io/article/3 — left-over covers what happens after the press release.