Ad Tech / Autopsy

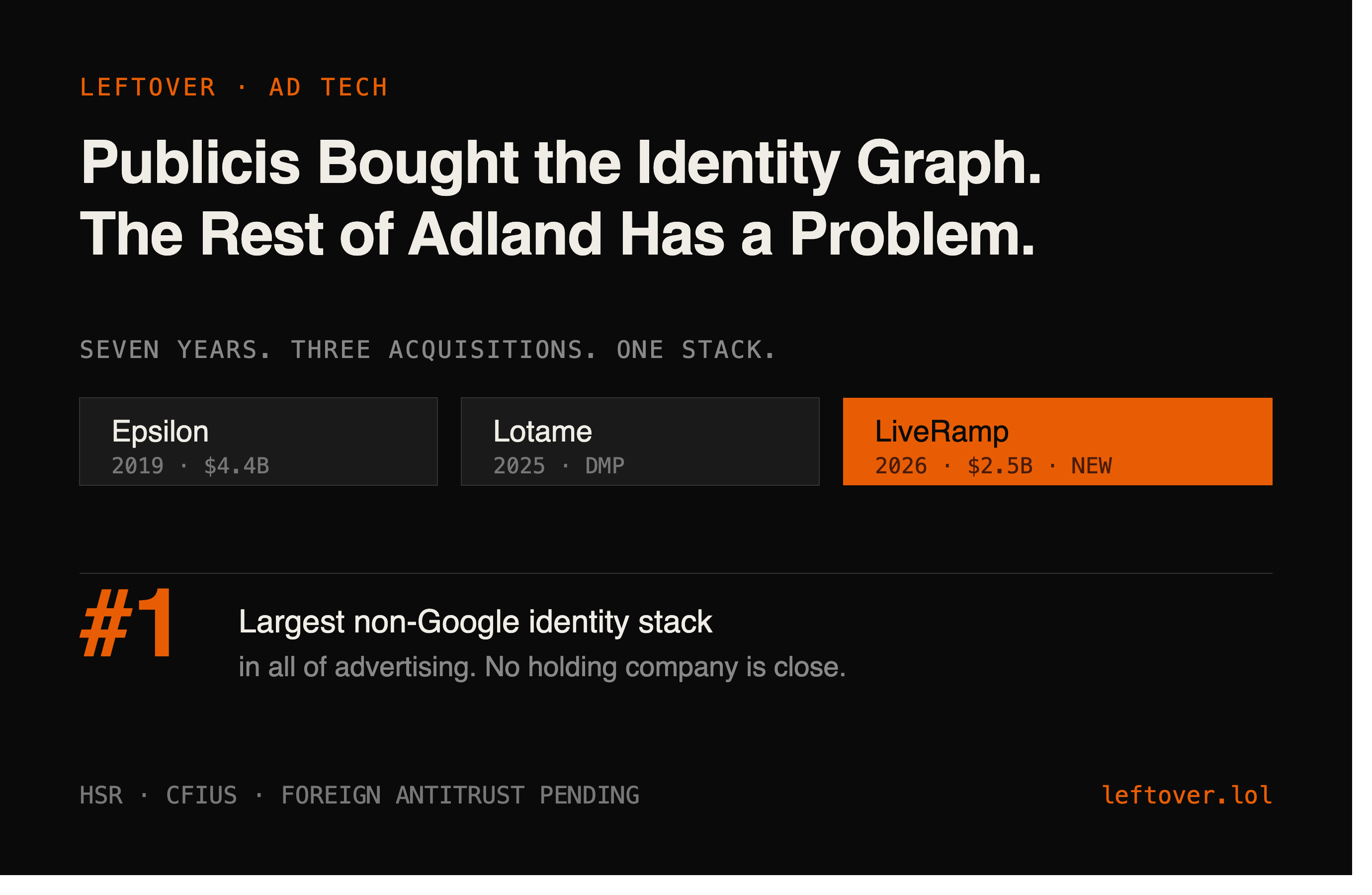

The $2.5 billion LiveRamp deal is quieter than Fox/Roku. It should not be. Publicis now controls Epsilon, Lotame, and LiveRamp: the three largest non-Google identity stacks in advertising. No other holding company is close. The question is whether that is a competitive advantage or an antitrust problem in slow motion.

When Publicis bought Epsilon for $4.4 billion in 2019, the industry noticed but rationalized it. Epsilon was a first-party data and loyalty business. One acquisition. Manageable. When Publicis picked up Lotame in early 2025, fewer people wrote about it. Lotame is a data management platform. Still manageable. Then on May 17, 2026, Publicis announced it was acquiring LiveRamp for $2.5 billion in an all-cash deal at $38.50 a share, a 30% premium to where the stock was trading.

Put the three together and the picture changes. Publicis now controls the identity resolution infrastructure that connects advertisers to consumers across cookieless environments, first-party data clean rooms, and publisher audiences simultaneously. No other holding company, and no independent ad tech player outside Google and Amazon, has that full stack.

Publicis made three neutrality commitments at announcement: no service restrictions, no pricing changes, no preferential agency access. Those commitments are not legally binding after close. Ask DoubleClick.

LiveRamp is not just another data company. It connects more than 25,000 publisher domains and 500 technology partners across 14 markets. Its authenticated traffic solution is embedded in the login infrastructure of publishers across the industry. The RampID is used by every major DSP and SSP to resolve identity in a post-cookie world. Whoever controls RampID controls a significant portion of how programmatic advertising matches buyers to audiences at scale.

The competitive reaction has been immediate. Madison and Wall wrote that rivals must decide whether to partner, build, acquire, or accept a weaker position across data, workflow, and transaction layers. Translation: Omnicom, WPP, and IPG are all now in emergency M&A mode. Every clean room company, identity resolution startup, and data collaboration platform just saw its valuation go up. That is the secondary market consequence of this deal that almost no one is writing about.

The regulatory path runs through HSR antitrust clearance, foreign antitrust filings across LiveRamp's 14 international markets, and a CFIUS national security review. The CFIUS requirement is not standard for an ad tech deal. It signals that LiveRamp's cross-border flows of consumer behavioral data triggered a flag inside the Treasury Department. That adds an unpredictable timeline layer with no public-facing process. Meanwhile, Publicis settled FTC collusion allegations involving agency holding companies as the deal was announced. That FTC settlement is active context for HSR reviewers.

LiveRamp will operate as an independent business within Publicis, and CEO Scott Howe will stay in place. Publicis pointed to its handling of Epsilon as the model for how it runs acquired businesses. But Epsilon today is not the independent company it was in 2019. It is deeply integrated into Publicis Sapient workflow and sold primarily through Publicis agency channels. The independence pledge is a starting position, not a destination.

Full interactive version: leftover.io/article/5 — left-over covers what happens after the press release.