Analysis

Cable was a forty-percent-margin business with two income streams and almost no churn. Then the people who ran it decided to rebuild it from scratch, at lower prices, with higher acquisition costs, and thinner margins. We are still doing the math.

Cable television was, for about thirty years, one of the greatest money-printing machines in American business history. And then the people who ran it looked at that machine, studied it carefully, and decided to blow it up. On purpose. With their own hands.

We are still living in the wreckage.

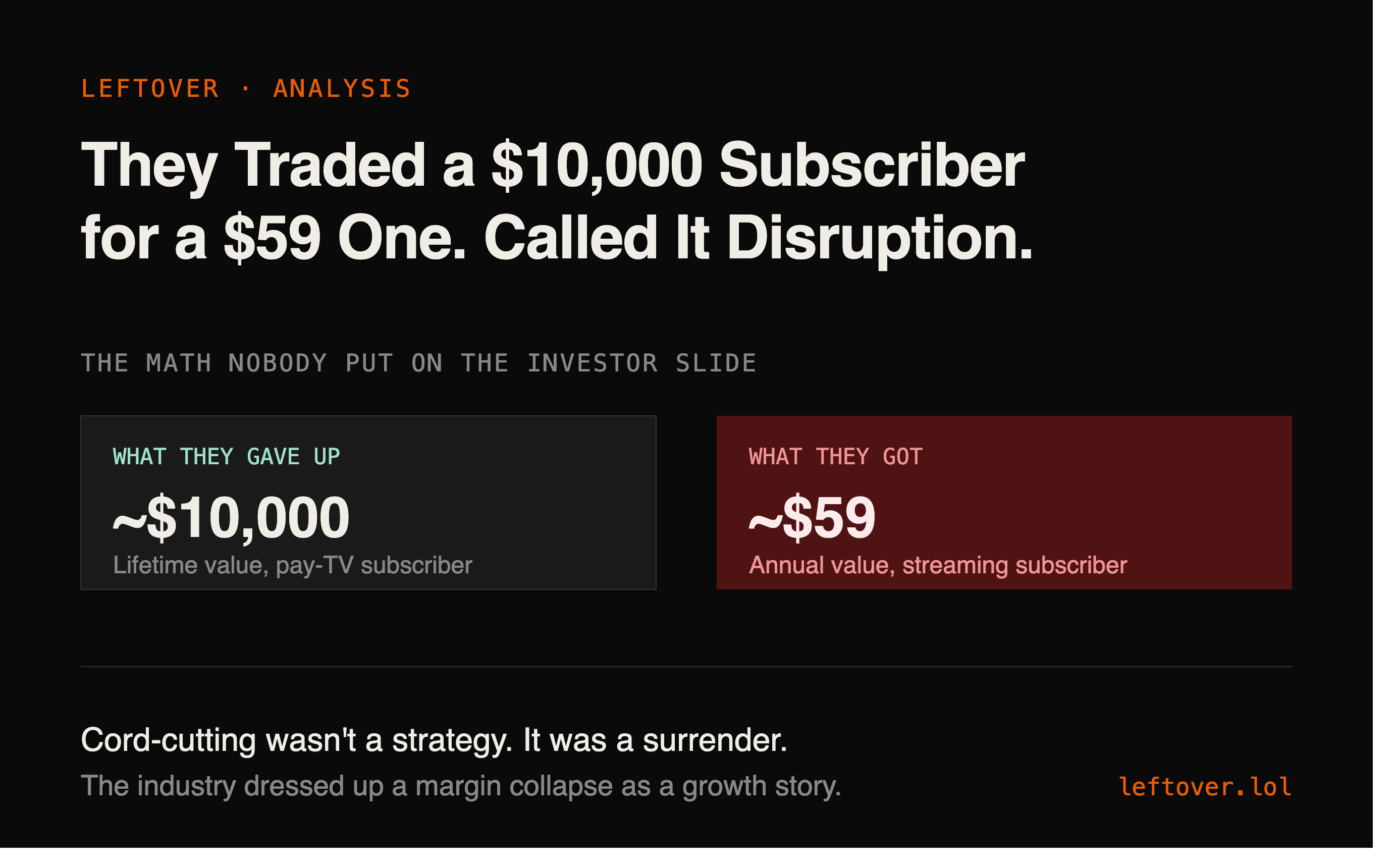

At peak cable, roughly 2010 to 2014, the average U.S. subscriber was paying $90 to $100 a month. Most stayed for five to six years. That works out to somewhere around $6,500 to $10,000 in revenue per household before they ever thought about canceling. And most never did, because leaving cable meant also losing your internet connection, and nobody wanted to deal with that particular afternoon.

But here is the part people forget: the monthly bill was only half the money.

Cable channels also collected something called affiliate fees, which were per-subscriber payments from the operator just for being in the bundle. ESPN got them. The Food Network got them. The channel that only airs fishing competitions at 2am got them. Every network collected, every month, whether anyone watched or not. It had nothing to do with ratings or ad revenue or whether your flagship show got renewed.

Two income streams on a single customer. Captive audience. Low cancellations baked in by sheer inconvenience. Profit margins around 40%.

It was almost unfair.

The thinking, circa 2019, went something like this: Netflix is growing, younger viewers are bailing, the bundle is dying eventually, so let us get ahead of it. Launch a streaming service. Own the subscriber directly. Cut out the middleman. Easy.

What the strategy decks missed is that the bundle was never just a distribution tool. It was the thing keeping subscribers from leaving. And when you stepped outside it, you did not just lose the cable bill. You lost the affiliate fee. Permanently. One network executive, when asked about building their own streaming service, said they assumed affiliate fees would not be part of the business model from day one.

That quote is doing a lot of work.

Think of it this way. A cable subscriber in 2012 was basically a small annuity. They paid reliably, stayed for years, and the network collected ad money on top of that. Lifetime value per customer was well into the thousands.

A streaming subscriber today is closer to a first date that ghosts you. Monthly churn across the industry has climbed from about 2% in 2019 to over 5% by early 2025. Nearly half of subscribers cancel at least one service per year. For a platform charging around $9 a month, the average customer is worth roughly $59 before they disappear.

That is not a typo. Fifty-nine dollars. The price of a decent dinner.

And it costs platforms upwards of $50 just to acquire that subscriber in the first place. So the math on the whole thing is, charitably, tight.

For Netflix, yes. First mover advantage, years of runway before the competition showed up, and enough habitual lock-in built over time to keep churn low. They are the only major streaming service that is consistently profitable without a bigger company covering the losses.

For everyone else, the results have been rough. Disney+ spent years burning through cash. Warner Bros. Discovery took on enormous debt and has spent a good portion of its existence canceling shows it already paid to make. Pay TV revenue peaked at around $101 billion in 2014 and is now projected to fall below $54 billion by 2027.

The industry's response to all of this has been to quietly rebuild what they tore down. Ad-supported tiers. Bundle packages. Multiple services discounted together. They are, with considerable seriousness and a steady stream of press releases, reinventing the cable bundle they spent a decade destroying.

The original machine is not coming back. But at least we are getting a smaller, more expensive, slightly worse version of it.

Full interactive version with charts: leftover.io/article/6 — left-over covers what happens after the press release.